- Loans: money that is borrowed and repaid to the lender, often with interest.

- Grants: money that is given to you, much like a scholarship.

- Work Study: a program that takes money off your bill if you take anon-campus job such as being a teaching assistant or working in the dining hall.

- You may see all 3 of these terms, as well as scholarships, on your financial aid package. Your financial aid package is prepared for you based on your FAFSA information and your college application. If you haven’t already completed FAFSA, here’s a linkto our guide. As long as you’ve filled out your FAFSA and your application, you’re automatically considered for all of these financial benefits, including federal loans and grants.

- Your financial aid package includes:

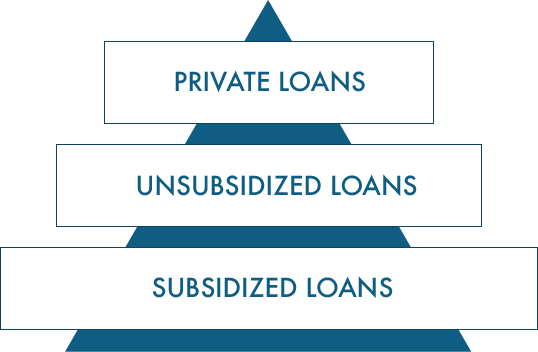

- Subsidized loans: federal government loans that don’t rack up interest while you’re still in school (these are the most favorable loans and should be taken first).

- Unsubsidized loans: federal government loans that DO rack up interest while you’re still in school.

- For subsidized and unsubsidized loans: your allowance will grow over the next 4 years. You might have to seek other loans in addition to these at first but eventually your subsidized and unsubsidized loans will cover a bigger and bigger portion of your expenses.

- Any scholarships you were automatically awarded during the application process (these don’t require applications; they use your college application to evaluate you for them).

- Grants: these are usually special or federal offerings based on special circumstances or need. The most common one is the federal Pell Grant which is given to students that demonstrate significant need and doesn’t need to be paid back.

- Estimated family contribution: This is a number that FAFSA comes up with and the school uses to determine how much of your remaining costs your family can afford to pay out of pocket. It’s usually a big sticker shock to see what FAFSA thinks your family contribution should be, but that’s normal. If your family contribution looks ridiculous then you’ll probably need to apply for other loans such as a Parent PLUS loan.

- The traditional estimated expenses for the school.

- You have all these additions and subtractions, now what?

- The financial aid package likely does this for you, but you should manually add up the expenses and benefits. All of your benefits, scholarships, loans, grants, family contribution, and work study credits will be positive while the school expenses will be negative.

- The only aspect of the equation that is out of pocket and is significant to you or your parent’s current financial situation is the family contribution. If they list the family contribution, it will likely be the amount of money needed to cover the expenses after your benefits are taken out. If they don’t list it, then you owe nothing or the sum of your benefits and expenses will be negative and that number will be your family contribution.

- If your family contribution is too much money for you or your parents to afford, then it’s time to apply for more scholarships or take out an external loan.

- There are all kinds of special loans like the Parent PLUS loans (an additional federal loan) and private bank loans. What you want to look at is the restrictions on who can apply for them and the interest rates. The interest rates usually come in a range based on your family’s credit rating. What you’re looking for is the lowest possible interest rate to reduce the total amount of money you owe to the lender. You might also see a difference in fixed vs. variable rates. Fixed rates are better if market interest rates are at a relative low point and variable rates are good if market interest rates are at a high point and show evidence of declining. If you’re not experienced with fixed and variable interest rates, it’s usually safest to go with a fixed rate so you know for sure that’s what you’ll be paying.Once you find one, you’ll have to fill out their application and wait to see if you get accepted. If you keep getting denied, it’s usually based on credit. This means you’ll have to take out a higher interest loan because in the loan distributor’s eyes, you appear to be a risk, so you need to offer more interest to them for it to be a profitable exchange.

- Once your benefits and expenses are balanced and your family contribution comes out to a reasonable number, you’re all set. You can accept your financial aid package and choose what portion of the subsidized and unsubsidized loans you want to use. You’ll likely have to fill out a Master Promissory Note (MPN)to complete the process. This is a legal document where you accept the terms and conditions of your loans and agree to face the consequences of not paying them back in a timely fashion.

- You aren’t required to accept any loans.If you want to decline the loans and pay out of pocket, then you’re free to do so. Likewise, if you want half of the offered loans or you only want the subsidized loans, you can do that as well.

- Be sure to keep up on when your financial aid needs to be renewed. FAFSA needs to be filled out once a year, which your school will remind you of. This covers scholarships, federal loans, grants, and more items. The other renewal you need to watch out for is private loans,as they might follow a different schedule.

- Loan quality looks like this, from most favorable to least favorable in terms of interest and risk: